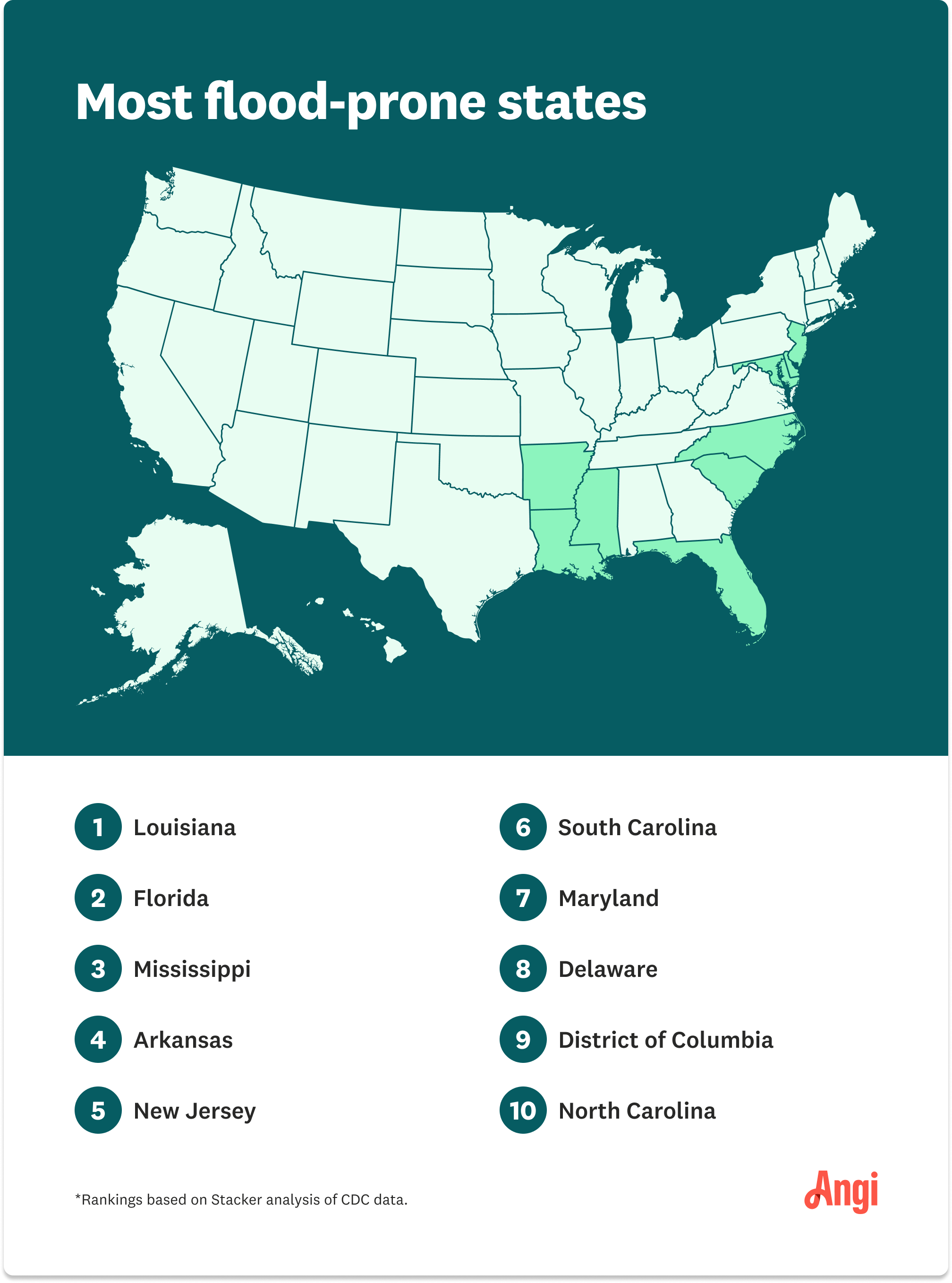

What You Need to Know About Buying a House in a Flood Zone

Is it worth the risk?

A flood zone is an area designated by FEMA to be at high risk for flooding.

You can find out if your home is in a flood zone by checking FEMA’s map.

The potential dangers of living in a flood zone include flood damage, high flood insurance premiums, and difficulty selling your home.

The sound of waves lapping against the shore is a perk many people would love to have. But the sound of water flooding into the basement? Not so much. According to the Federal Emergency Management Agency (FEMA), one inch of water can cause up to $25,000 worth of damage to a home. So is buying a house in a flood zone worth it? Here’s what you should know before signing on the dotted line.

What Is a Flood Zone?

A flood zone is an area that FEMA has designated to be at risk for flooding. FEMA classifies them as Special Flood Hazard Areas (SFHAs) or Non-SFHAs throughout the country.

Special Flood Hazard Areas (SFHAs): High-Risk Zones

You should add “checking the flood zone code of potential new houses” to your home-buying checklist. According to FEMA, high-risk zones in SFHAs have a one in four chance of flooding at some point during a 30-year mortgage. FEMA classifies all homes as in or out of flood zones; the way you can tell is by the letter at the beginning of the flood zone code. If the home’s flood zone code starts with the letter A or V, it’s in a high-risk flood zone.

Moderate-Risk Zones

Non-SFHAs are further divided into two groups: moderate-risk and minimal-risk zones. In moderate-risk zones, there is a chance your house may experience some flooding, though it’s less likely than in SFHAs. The flood zone codes for these areas are Zone B or Zone X. Moderate-risk areas labeled Zone X are also shaded.

Minimal-Risk Zones

In minimal-risk zones, the odds of your home flooding are slight. However, flooding may still occur in some cases. Houses in these areas are coded Zone C or Zone X and unshaded.

How Can I Find Out If a House Is in a Flood Zone?

The Flood Map Service Center from FEMA is an easy-to-use site where you can enter your address to find out if your home, or a home you’re considering buying, is in a flood zone. If you’re house hunting, make a note on your house hunting checklist to ask your real estate agent about the home’s flood zone designation. Your real estate professional should be able to tell you the designation and any history of flooding.

Can You Get a Mortgage for a Flood-Zone Home?

The answer is absolutely, and the process is the same as obtaining a mortgage for a home that’s not in a flood zone. However, many mortgage companies will require you to carry flood insurance before approving you for financing. If you have an FHA loan, a government-backed loan, or a loan backed by Fannie Mae or Freddie Mac, you’ll need to carry flood insurance or risk having your loan canceled.

Risks of Buying a House in a Flood Zone

Buying a home in a high-risk flood zone comes with several risks that you should keep in mind when house hunting.

Flood Damage

If your home floods, you’ll have to deal with the fallout of flood damage, ranging from structural issues to mold infestation. Physical damage from flooding varies in severity depending on the duration of the flood and the force of the water. Faster flood waters that rush into your home cause more damage than gradually rising water levels. And the longer the water remains in your home, the worse the damage will be.

Even if you took deliberate steps to build a flood-proof home or made upgrades to mitigate your risks, there’s no way to make your house 100% flood-proof. And minor flooding can still have devastating effects. You may have to deal with flood damage like:

Damage and loss of personal property, like clothing, books, furniture, appliances, and other valuables

Structural damage to the foundation, floors, walls, ceilings, and roofs

Damage to electrical and plumbing systems

Water contamination

Mold infestation

If the damage is severe, you may not be able to use parts or all of your home until it can be made safe again. Repairs can be pricey too. Water damage restoration costs usually run between $1,300 and $5,800, and mold remediation costs are typically around $2,200.

The emotional cost of flooding can feel just as disastrous as the financial cost. These costs are difficult to quantify, but the possibility of losing all your belongings or being displaced from your home can take a toll on you and your family’s well-being.

High Flood Insurance Premiums

Regular hazard insurance does not cover the cost to repair flood damage. If you live in a risky area, you’ll need to get a special flood insurance policy to cover flood damage. Premiums for flood insurance average about $700 per year, but that cost can vary based on flood risk, deductibles, and more.

Difficult to Resell

Living in a flood zone can decrease your home’s value and make it more difficult to resell your house. Damage from flooding can cause your property value to drop, but just being located in a higher-risk zone can lower resale value—even without any damage. And even if you’ve repaired all the damage, buyers may be less likely to make an offer if they know there has been flood damage in the past.

Though you may not mind living in a high-risk flood area, you may have a hard time finding potential buyers if you decide to sell your house. Some buyers don’t want to deal with the possibility of flooding, no matter how much they love the home. Add on the cost of insuring the house, and you could be stuck in a situation where your home sits on the market for longer than expected.

Ways to Reduce Safety Risks When Living in a Flood Zone

While there are some serious drawbacks to buying a house in a flood zone, there are a few advantages. Many homes in high-risk flood zones are also waterfront properties. If the home is in your ideal neighborhood, you can assess the risk versus the benefit of living in the area and see if it’s worth it.

If you’re set on buying a home in a flood zone, there are some measures you can take to reduce your flood risk.

Keep gutters and storm drains clean and clear.

Elevate major appliances off the floor, including your furnace, electrical panel, and water heater.

Waterproof the basement walls.

Store your essential belongings in an elevated part of the house.

Know the number of a trusted water damage restoration pro near you, just in case.

Amy Pawlukiewicz contributed to this piece.

.jpg?impolicy=leadImage)

- 10 Tips for Building a Flood-Proof House That's Up to Code

- Flood vs. Spot Lights and How To Choose the Right Type of Outdoor Lighting for Your Space

- Water Damage Cleanup Guide: How to Restore Your Home Quickly After a Flood

- Water Damage Restoration Checklist: 8 Steps to Save Your Home After a Flood

- Understanding Gardening Zones: What Plant Hardiness Zone Am I In?

- 8 Home Inspection Deal Breakers That Should Make You Think Twice

- Kitchen Flooding? Here's How to Get Out of Hot Water Fast

- What to Do When Your Basement Floods From Rain: 11 Tips

- How to Keep Floodwater Out of Houses: A DIY Guide

- What to Do After Water Damage in Your House and Why Act Fast

Get our Angi-powered app